The greatest fear any federal should have about their retirement is running out of money. Yes, we understand that you have a wonderful pension and if you are under FERS, a Social Security check on top of that, BUT will that really be enough? The premise of our “80% Retirement Rule” is that on the day after a federal employee retires, they should have an income of at least 80% of what they earned on the day before their retirement.

The most common question we get is “why not 100%” and the answer is quite simple. Once you are retired, you will no longer be contributing to Social Security or Medicare, which accounts for 9% towards that 20%. Add to that the fact that you will no longer be able contribute towards your TSP, and that could add another 5%-to-8% towards the 20%. And most federal employees we surveyed stated that they will downsize a bit once they are retired. But let’s get back to running out of money.

Below is a chart that shows you how close to the 80% mark you will be (based solely on your pension), depending on the number of years of federal service you will have at retirement. A FERS federal employee with 30 years of service at retirement will be at either 30% or 33% (33% if they were 62 years old at the time) towards that 80% mark. If you add in approximately 25% for Social Security, that federal employee is only at 55% or 58% towards the 80%, leaving quite a gap in their financial safety at retirement. While CSRS federal employees seem to have a big advantage, most CSRS don’t have Social Security, so it’s pretty close if you add in the 25% Social Security unless of course you are CSRS with over 35 years of service at retirement.

CSRS FERS

20 Years: 36.25% 20 Years: 20% or 22%

25 Years: 46.25% 25 Years: 25% or 27.5%

30 Years: 56.25% 30 Years: 30% or 33%

35 Years: 66.25% 35 Years: 35% or 38.5%

40 Years: 76.25% 40 Years: 40% or 44%

42 Years: 80.00% Will never reach 80%

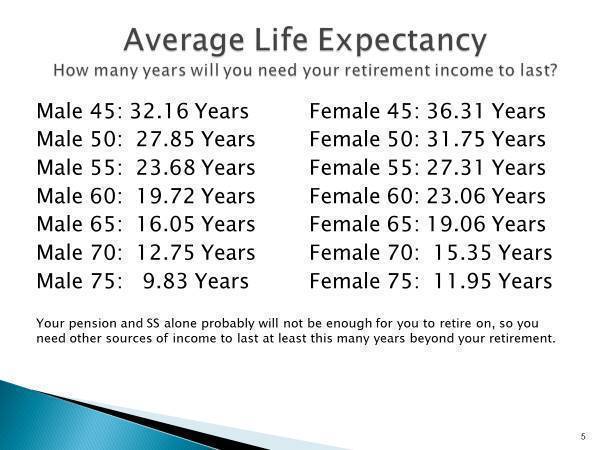

Life expectancy is a very important element in planning for your retirement, if you want to retire and stay retired. If you are only at 56% towards that 80%, then your savings and TSP have to last you for as long as you live. At age 65, that number is 16 years for a male and 19 years for a female. That’s a long time for your savings and TSP money to last, and if you keep your money in the C, S, I, F or L Funds after retirement, that money could go down significantly with just one stock market correction. And of course yes, there is a way to protect yourself from that ever happening, which we explain right below the chart.

Fixed Indexed Annuities allow you to participate in the upside of the stock market, without any of the underlying downside risk to your Principal. They also protect and “Lock-In” any of your prior contract gains from being “clawed back,” like they are with the TSP C, S, I, F and L Funds.

We did a little research and found one Fixed Indexed Annuity where the index earned 22% last year, again with no market risk whatsoever, and a “Non-Claw Back” feature. There are well over 200 different varieties of Fixed Indexed Annuities, so if you have interest, please send an email to info@federalemployeeadvocates.com (put Annuity Info Request in the Subject Line) and we will have an expert contact to explain in more depth which one of these Fixed Indexed Annuities will be right for you.